IFRS 17 has introduced the concept of fulfilment cash flows. Fulfilment cash flows are the building blocks of the general model.

Fulfilment cash flows consist of inflows and outflows, discounting and an explicit risk adjustment for non-financial risk. What remains after this calculation (if anything) is the CSM.

Let's take a close look at each component of the fulfilment cash flows.

Future cash flows

Future cash flows can be split into inflows and outflows.

Inflows are mainly premiums within contract boundary.

Outflows consist of:

- insurance acquisition costs,

- administration expenses,

- claims and benefit payments.

Future cash flows are discounted to calculate their present value.

Discounting

Discount rates should reflect the time value of money and the liquidity characteristics of the insurance contracts.

Discount rates should be consistent with the prices that we see in the market and with other financial assumptions.

In IFRS 17, two approaches can be used for calculating the discount rates:

- bottom-up approach,

- top-down approach.

The two approaches might lead to slightly different discount rates.

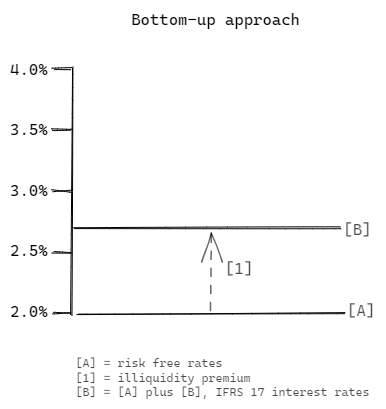

Bottom-up approach

In the bottom-up approach, we start with the risk-free rates and add an illiquidity premium.

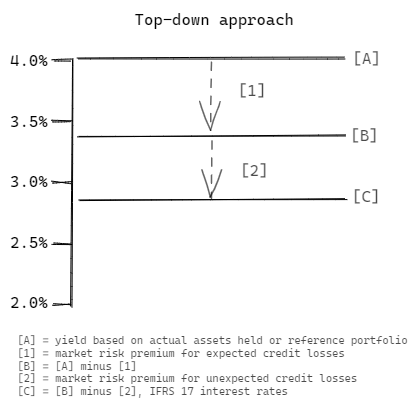

Top-down approach

In top-down approach, we start with the yield based on actual assets held or reference portfolio. We then subtract two elements:

- market risk premium for expected credit losses,

- market risk premium for unexpected credit losses.

Results of the bottom-up and top-down approaches should be close to each other. They don't have to be the same.

Risk adjustment for non-financial risk

Risk adjustment for non-financial risk is the amount the insurer charges for bearing the uncertainty over the amount and timing of cash flows arising from non-financial risk. Non-financial risks are for example insurance, expense or lapse risk.

Standard does not prescribe any particular methodology to calculate risk adjustment. Derivation involves management judgement. Various methods can be used to calculate it.

Factors that impact risk adjustment:

- frequency and severity of risk,

- contract length,

- probability distribution,

- claims experience.